Do customers know what information banks collect about them?

What kind of customer information does the financial monitoring department of Ukrainian banks collect? How do banks decide to open an account, provide a loan, or even coordinate a transaction?

The Law of Ukraine on the Prevention of Money Laundering and the Financing of Terrorism obliges banks to verify customers and the origin of their funds. However, the internal verification process remains at the discretion of the banks themselves. According to the law, risk criteria are determined by internal documents of the banks, and what exactly they include is usually a mystery to customers.

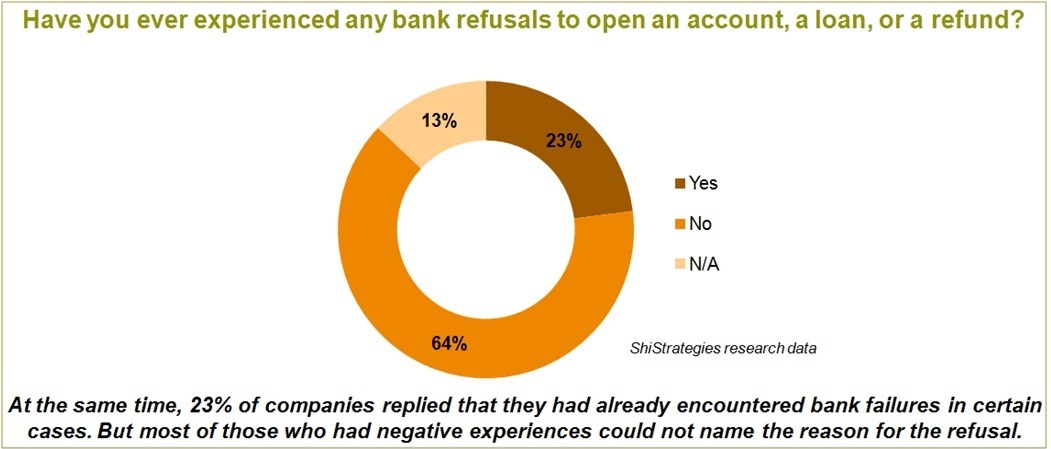

The Agency for Strategic Solutions ShiStrategies, together with the editors of the Financial Club, surveyed enterprises and commercial institutions of various sizes and industries. The goal is to find out if entrepreneurs know how their bank makes decisions on granting loans, opening accounts and conducting operations? 41% of respondents said they did not know or did not answer at all. 59% thought they knew. However, deeper personal interviews with business representatives showed that their ideas about the volume and nature of the information monitored by banks are far from complete.

At the same time, 23% of companies replied that they had already encountered bank failures in certain cases. But most of those who had negative experiences could not name the reason for the refusal.

We also interviewed representatives of Ukrainian banks of various sizes and forms of ownership to find out exactly what information they are studying and how it affects decision-making.

We found that, without exception, all the banks surveyed questioned not only the operations of clients defined in Art. 15 and 16 of the law, but also those that were deemed suspicious by internal risk criteria, in particular transactions that do not correspond to the financial situation or the content of the client's activities. One of the banks said that it checks all transactions without exception, which are equal to or exceed 150 thousand UAH.

Why is financial monitoring necessary?

Oddly enough, despite the existence of the law, there is no unambiguous understanding of the purpose of financial monitoring in the market.

In addition to countering money laundering and terrorist financing, banks, defining the goal, called for much more. In particular, 88% said they stopped transactions that could cause a fine on the part of the regulator.

The same amount is monitored to prevent transactions having signs of illegal entrepreneurial activity, although this is a matter of tax evasion. Besides, more than half of bankers consider it one of their direct tasks to identify schemes to minimize tax obligations, including using low-tax jurisdictions. Thus, banks took over the powers of regulatory authorities, although the law does not require them.

The absolute majority of financial institutions among the tasks of financial monitoring called screening out customers who are likely to violate the law (any), as well as those that could adversely affect the reputation of the bank.

In general, as we see, banks have a much broader view of the tasks of internal financial monitoring than the regulator requires.

Recently, speaking at the Ukrainian Financial Forum 2019, organized by the ICU group, Ekaterina Rozhkova, deputy chairman of the National Bank of Ukraine, condemned this understanding of financial monitoring functions, calling the control by banks excessive.

"Now there is no understanding of how financial monitoring works in terms of revenue verification. It is a question of a distorted understanding of how the law works. If a person has worked all his life in this country, has an average income level, has an apartment, a small car and owns 100-200 thousand UAH of a deposit, then he should not be asked to bring the entire chronology of actions for his whole life. We will teach everyone - both bankers and traders. Because the task of the law "On Prevention and Counteraction of Money Laundering and the Financing of Terrorism" is aimed precisely at this, and not at counteracting the population's investments in securities or opening deposits," she emphasized.

However, according to Andrey Zolotukhin, managing partner of Ozon Capital, in such a thorough analysis, Ukraine is no exception to the rule. "The Know your client procedure has existed in the West for a long time. The trend there is the same as here. The number of documents required by banks is increasing annually. It seems that if this trend is not stopped, then you can just come to a standstill. Therefore, the thought of our regulator that we need to stop somewhere is very pleasing," he commented on the words of Ekaterina Rozhkova.

Where do the regulator's demand end and the bank's initiative begin?

The law gives banks the right to establish rules for internal financial monitoring, and, according to the regulator, sometimes banks abuse it. Bankers, in turn, attribute the excessive caution to the threat of fines by the NBU.

According to the Chairman of Alfa-Bank’s Board Victoria Mihayle, the root of this conditional confrontation lies in the fact that the National Bank takes control of operations, while it should focus on the control of banks ’compliance systems.

“Today, the regulator’s approach to financial monitoring does not end anywhere and the bank’s approach does not begin, as the bank is developing a policy one way or another. Unfortunately, we have problems with the regulator, because there are schemes, problem operations that are not written out by the regulator. In the past three years, the regulator has relied on professional judgment. It must be understandable or meet certain criteria that exist in this market. Therefore, the number of lawsuits from banks based on inspections and financial monitoring suggests that banks strongly disagree with the regulator's approaches. The bank has its professional judgment, and during the audit, which takes place three years after the decision is made, the regulator, based on market practice, sees everything differently, ” she emphasizes.

A new bill on the prevention of money laundering, which was adopted in the first reading on November 4, is called to partially solve this problem. “This bill has answers to questions, it details the details of approaches. At the same time, this document already directly obliges banks to be guided by a wider data set than the USR. And the question of reputation will remain. This is not required by the National Bank or the government, this is what the development path of the Western world requires,” said Nikolai Stetsenko, managing partner of Avellum Partners.

Which customers are not welcome at the banks?

If before banks sought to attract primarily solvent customers, today very different qualities have become most important: transparency, law-abidingness, and reputation.

All interviewed banks noted that they would not deal with citizens whose incomes do not correspond to expenses and companies whose transactions do not correspond to turnover. Everything that is out of the norm is suspicious.

Attention is also drawn to the nature of transactions: if there are signs of entrepreneurial activity being carried out “past the checkout”, two-thirds of banks are ready to stop such a transaction.

Also, unanimously, banks do not want to deal with legal entities whose final beneficiary cannot be established, or if he (the beneficiary) has the citizenship of a country referred to offshore zones by a government decree. 94% of banks additionally noted that even operations with counterparties registered in these zones are considered a risk signal. Moreover, half of them consider the company risky, even if information about offshore contractors is not confirmed by official documents, but only was published in the media or social networks.

Three-quarters of banks consider companies with counterparties in Russia suspicious. According to half of them, data from the media and other unofficial sources is enough to draw a conclusion about cooperation with Russians and refuse to cooperate.

In general, judging by the survey, banks are willing to take into account publications on the activities of companies from the media and other informal sources. In particular, 63% of banks replied that they pay attention to publications about the legal entity’s relations with counterparties who were suspected or accused of cases of money laundering or terrorist financing. 81% of banks - on publications with allegations of corruption, 50% - on allegations of fraud.

As it turned out during the study, most banks can refuse to service even valid customers due to negative publications in the media and social networks.

Talking about your business successes in interviews with the media and social networks now also costs only after paying taxes - almost half of the bankers surveyed said that they were looking for signs of illegal entrepreneurial activity there.

Important in this matter is not only how wide the range of risks the bank evaluates, but also how much the views on risks and the mechanisms for identifying them differ in different financial institutions. Faced with different requirements, customers are distrustful and go into a defensive position, says Lada Krimerman, Managing Partner of HLP Group.

“These studies very clearly indicate that the dialogue between business and banks is absent. A lack of understanding of the rules of the game by customers gives rise to a desire not to disclose information and to conduct some kind of aggressive policy towards banks. All the promises of banks come down to the fact that they must understand and know the client. But the system should be such that the business also understands how they study it and what they know about it. The business must be sure that the bank’s decision regarding the client is not based solely on the subjective opinion of a particular employee. A business study system should be understood by both banks and companies. Indeed, today the same client fills out the same questionnaire, outlines the structure of his business the same way, and as a result, they say “welcome” to him in one bank and “sorry” in another,” she notes.

Customer Monitoring Sources

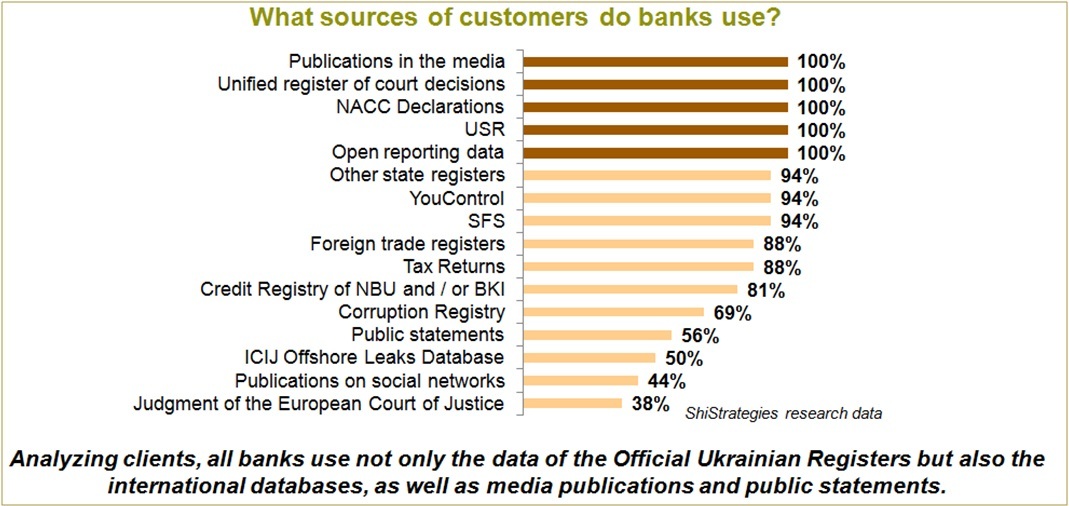

Some sources on which the bank relies when analyzing the business of customers are obvious - this is the Unified State Register of Legal Entities (USR), reporting data, register of court decisions and declarations on the NAZK portal. Of course, all banks use this data. 92% of banks use open data from the tax service and other government agencies and registries. YouControl analytical platform is also in the arsenal of almost all financial institutions.

It is expected that the tax returns of the founders, the credit register of the National Bank, the Bureau of credit histories and the state register of offenders are used for analysis.

It was a surprise that absolutely all bankers use information about customers in the media, and 44% of the sources also noted publications on social networks. More than half take into account public statements of both company officials and third parties regarding customers. Therefore, we can confidently say that media today are becoming more important and can significantly affect the business, including limiting its access to financial resources.

Explaining their position regarding the use of unofficial open sources, some bankers noted that the information obtained in this way is only the basis for an internal investigation, which should provide official evidence of the facts.

“The media is an alternative source, we turn to the media only when we have doubts. This is an occasion to ask the client additional questions. Unfortunately, in our portfolio, there are cases with court decisions, when dear customers dispute media publications (which had negative consequences) and disclose information to the bank. There are precedents because if you do not manage your reputation, others will do it for you. Nevertheless, this is only a signal to turn to other sources of information. Although it is unlikely that we will seek information on some kind of FLP in the media, there are other indicators there,” Victoria Mihayle explained.

Sergei Naumov, chairman of the board of Piraeus Bank, said: “Information in the media is a flag that rises. For us, it is not the final point in cooperation with the client, it is rather an occasion to ask questions of the company. And it would be nice if the business, like banks, checked their counterparties so that in the future they would not become involved in criminal investigations just because they were doing business with someone. Indeed, such information immediately affects the image.”

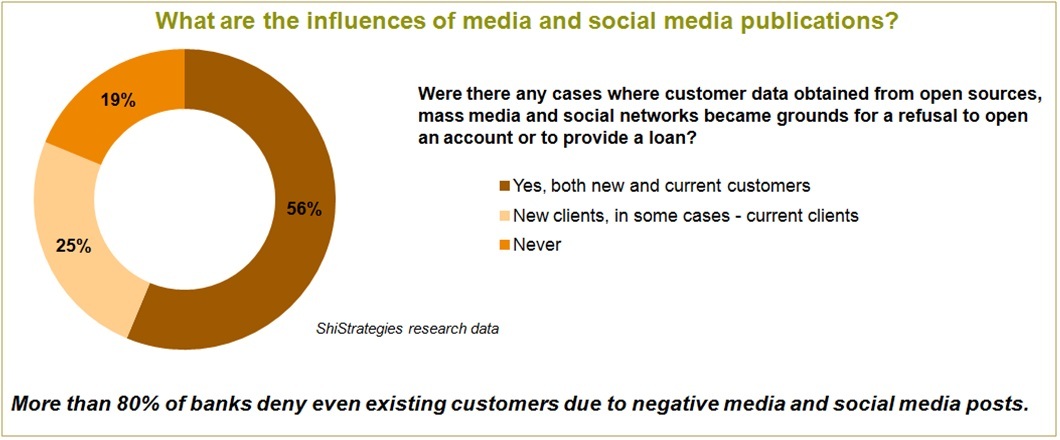

However, during the survey, only 19% of banks replied that publications in the media and other media never became the basis for denial of service. A quarter of respondents admitted that there were such refusals, but mainly concerned new clients. At the same time, 56% of banks noted that publications led to rejections of both new and already well-known customers.

Besides, banks monitor sources outside Ukraine. In particular, 88.7% of respondents collect data in trade registers of foreign countries. Half of the banks use the information of the international database of offshore companies ICIJ Offshore Leaks Database, 38% follow the decisions of the European Court.

We knew that the amount of information that banks collected was large, but we were amazed by how large it actually is. Analyzing the client, all banks use not only data from official registers, but also international databases, publications in the media and public statements.

Thus, the information processed by the bank covers not only the analysis of the economic activity of the client and its counterparties but also the analysis of the reputation of the company as a whole and its founders in particular.

Major Threats to Reputation

We asked representatives of financial institutions and their clients to rate on a 10-point scale the factors that most threaten their reputation. Both banks and businesses put the distribution of biased information and rumors in the first place, including in social networks. At the same time, the negative financial results in the list of reputation risks among banks fell only in fourth place, and among customers only in seventh.

Both sides fear the negative in the media, but for banks, the regulator’s assessment turned out to be more important. Business, however, considers conflicts with customers more dangerous - they are among the three largest threats. For banks, this figure is only in fifth place.

As you can see, the reputation of companies and banks is more influenced by the distribution of negative and biased information and rumors than unsatisfactory business results. At the same time, many companies and banks do not pay due attention to working with the media, communications with target audiences, during which a positive attitude towards their activities is formed. As practice shows, good performance does not guarantee a good reputation. Work without communication leads to rumors, speculation, which, according to the companies themselves, is the main threat. Therefore, it is so important to move from the practice of spontaneous formation of reputation to systemic management of it.

Relations between banks and customers, as well as relations between the NBU and banks, lack a clear understanding of the rules, obligations of the parties and systematic nature.

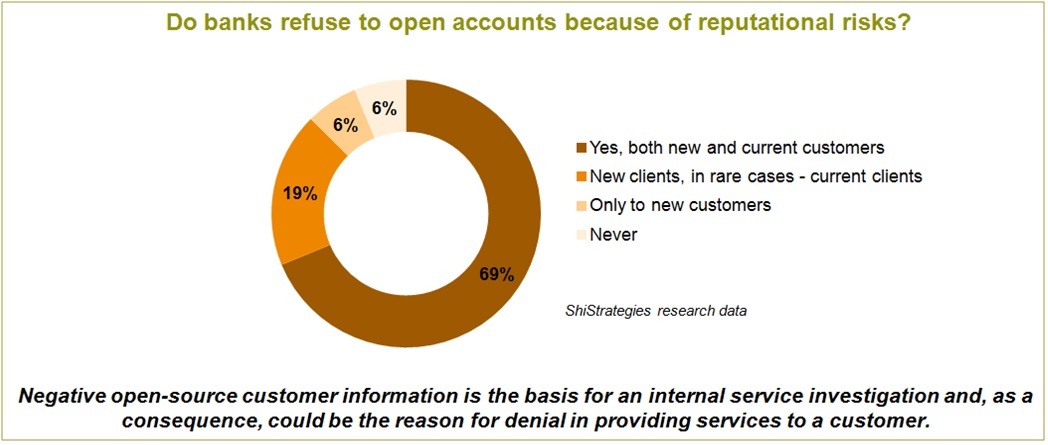

Now in a situation where banks care about their reputation, including in the eyes of the regulator, the negative reputation of the client can interfere with cooperation. So, 88% of banks reported that they refused to open accounts because of reputation risks. Therefore, bank customers should take this into account when formulating communication tasks and reputation management.

“Historically, the level of compliance among banks and companies is polarized, they live in different worlds. The companies pay attention to reputation from the commercial side, from the side of customer loyalty to their brand. But if the company requires external borrowing, the first requirement is to bleach the business. And companies do this, including under the influence of external factors,” said Tamara Savoshchenko, deputy chairman of the board of UkrGassbank. - The value of the reputation is growing, including ours, even though the attitude towards it in our country is somewhat different. Reputation is a value that every company should cultivate in itself and which we should strive for."

Reputation Price

In addition to direct losses or preferences in operating activities, reputation directly affects the value of the business, goods or services that it offers to consumers. According to Western studies, in the structure of business value, starting with the average, reputation can take from 20% to 90%. Accordingly, it directly affects the stock prices of companies, and often more than financial results. The reputation of its owner and / or top management is closely related to the company's reputation. There are frequent cases when a scandal or prosecution of managers collapsed the company's stock price by tens of percent.

It is not surprising that companies from developed countries pay serious attention to issues of reputation management. In large companies, a whole staff of PR specialists, lobbyists and lawyers are engaged in it. At the same time, companies determine the circle of stakeholders whose opinion is most important for building a reputation. It can be consumers, suppliers, government agencies, journalists, experts, even society as a whole - in each case, the circle of the most important stakeholders is determined individually. Reputational risks are identified, and measures are being developed to prevent or mitigate them. Further, communication channels with the most important audiences are defined or created through which the most important messages for the company are broadcast. If the company's reputation is formed and well managed, even serious threats cannot do irreparable harm to it. Large companies are more willing to make tangible business losses than reputational losses. Examples with the withdrawal of products for multi-billion dollars or with the abandonment of marketing strategies in which the appropriate funds have already been invested are quite eloquent.

And what about Ukraine?

Domestic business is mainly only beginning to understand the value of such an ephemeral asset as a reputation. And the companies that deal with Western partners or consumers were the first to feel it. For foreign contractors, the question “How is your business perceived in your country?” often turns out to be more important than the expected percentage of profit. After all, the reputation of your counterparty directly interacts with your own and can significantly spoil it.

Therefore, the deeper Ukraine will integrate into the global economic space, the more valuable will be the opinion that is formed about business in society. The time is already far behind when about half of Ukraine’s trade was ensured by trade with the Russian Federation, where reputation issues, like ours, were far from the first place. Today, modernization of the management system has covered almost the entire large Ukrainian business and a significant part of the middle. Competition for consumers, for professional workers, for access to cheaper investments is intensifying ... In such circumstances, building a reputation management system and managing reputation risks becomes no less an obligation for companies than raising finance, updating production or expanding the range of goods and services.

“Our experience with 6.5 thousand complaints suggests that companies need to work with a reputation. Reputation equals sustainability and profitability. This is the basis of the next development steps, it is an increase in the number of customers and an increase in revenue,” said Tatyana Korotkaya, Deputy Business Ombudsman.

If you care about your reputation or lose, the one who first adopts this simple rule will get tangible business benefits.

Inna Shinkarenko, Maria Stasenko for the Financial Club